TEST AREAS

“GROUP ACCOUNTING & REPORTING”

A Swedish-language test in IFRS-based group accounting and reporting, focused on operational consolidation execution and QA. Covers consolidation boundary decisions, eliminations and group adjustments, acquisitions/PPA quality checks, FX translation basics, and disclosure-quality reviews.

Consolidation: Control & Scope (operational)

Assessment of the candidate’s ability to make practical consolidation boundary decisions and to identify what information is missing to reach a robust conclusion. Covers IFRS 10 control in an applied setting (power over relevant activities, variable returns and linkage), de facto control considerations, substantive vs protective rights, and typical boundary cases between subsidiaries, associates and joint arrangements (IAS 28/IFRS 11). The focus is on operational “scope memo” judgement and QA, rather than memorising rule text.

Acquisitions: PPA, Goodwill & NCI (operational QC)

Testing the candidate’s ability to work with purchase accounting outputs in practice: validating consideration and fair value adjustments, distinguishing separable intangibles vs goodwill, and understanding deferred tax effects in PPA (IAS 12). Also covers goodwill impairment logic (IAS 36) through workpaper QC, focusing on identifying incorrect assumptions/calculations and selecting the correct treatment at a decision level, rather than rare edge-case scenarios.

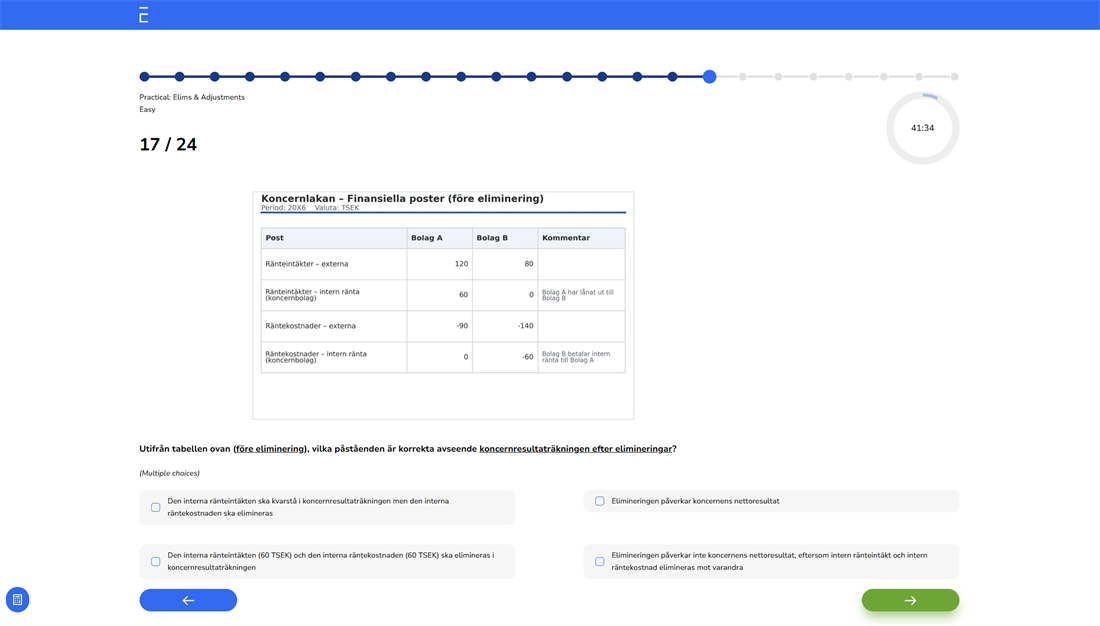

Practical: Eliminations & Adjustments (core operational capability)

Measures hands-on group reporting capability: elimination of intercompany balances and transactions, intra-group margins (inventory and fixed assets), depreciation effects, treatment of intra-group dividends and interest, and deferred tax effects on eliminations. Emphasis is on correct group adjustments, cut-off accuracy (delivery vs invoice), and the ability to spot missing or incorrect eliminations in consolidation schedules and report packages.

Ownership, FX & Disclosures (applied events & disclosure-quality)

Assesses applied reporting judgement in common group events: loss of control mechanics (IFRS 10) with retained interests (IAS 28), FX translation and CTA presentation/recycling on disposal (IAS 21), and disclosure-quality awareness for subsidiaries/JVs/associates (IFRS 12). Focus is on QC of what is recorded and disclosed (what is missing, inconsistent, or incomplete) rather than highly specialised corporate action structuring.

TEST QUESTIONS

Multiple Choice

Our tests are mainly based on multiple-choice questions where the number of correct answer options varies. Each question has four answer options.

Questions by Area and Difficulty

The tests are divided into four question areas and questions are categorised into three difficulty levels: easy, intermediate and difficult.

Randomised Test Generation

Questions within each area and difficulty level are randomly selected from a question bank, ensuring that each test receives a unique set of questions. Additionally, the order of answer options is randomised so that the correct answer for each question never appears in the same position.

24 Questions and Multimedia Options

A total of 24 questions are generated and must be answered within 45 minutes. During the test, candidates can skip questions and come back to them later. They also have access to a timer and a progress indicator. The test will automatically close when the maximum time limit is reached.

Test questions and answer options can consist of text, images, or a combination of text and images.

Example Question