TEST AREAS

"ACCOUNTING FROM A TO Z"

Test in Swedish on Swedish GAAP. Designed to distinguish senior accountants and client-facing specialists in accounting firms with broader reporting and advisory responsibilities.

Bookkeeping

Covers recording of supplier and customer invoices, including credit and debit notes, representation expenses with correct documentation, payroll transactions including tax and social charges, accrued vacation pay, foreign currency transactions with reverse charge VAT, and correcting incorrectly posted entries including reversed debits and credits.

Closing of Accounts

Covers the closing process for VAT and tax accounts, accruals and deferrals of supplier and customer invoices, use of interim accounts, inventory valuation, computation of taxable income versus accounting result, and accounting for both anticipated and confirmed customer losses.

Fixed Assets & Accounting Theory

Covers concepts such as depreciation and impairment of tangible and intangible assets, economic vs. physical useful life, and when low-value assets may be expensed. Also includes core theoretical principles like accrued and prepaid items, the matching principle, and the structure and interpretation of cash flow statements using the indirect method.

Financial Statements & Analysis

Covers core components of the income statement and balance sheet, including equity, short-term liabilities, appropriations and deferred taxes, as well as analytical skills such as calculating solvency and debt ratios, return on equity (adjusted for untaxed reserves), and deriving inventory purchases through statement reconciliation.

Accounting Practice in Client-Facing Roles

Covers practical aspects of working as an accounting consultant, including understanding filing deadlines, handling dividend advice in owner-managed companies, interpreting engagement letters and balance sheet equity, assessing compliance risks, and responding to client questions about leasing, capital adequacy or regulatory obligations. Emphasis is placed on judgement, communication, and regulatory awareness in assignments for small and medium-sized enterprises (SMEs).

TEST QUESTIONS

Multiple Choice and Manual Entry Questions

Our tests are mainly based on multiple-choice questions where the number of correct answer options varies. Each question has four answer options. Some questions require manual recording of a business transaction, and the candidate is provided with a chart of accounts for assistance.

Questions by Area and Difficulty

The tests are divided into four question areas and questions are categorised into three difficulty levels: easy, intermediate and difficult.

Randomised Test Generation

Questions within each area and difficulty level are randomly selected from a question bank, ensuring that each test receives a unique set of questions. Additionally, the order of answer options is randomised so that the correct answer for each question never appears in the same position.

30 Questions and Multimedia Options

A total of 30 questions are generated and must be answered within 45 minutes. During the test, candidates can skip questions and come back to them later. They also have access to a timer and a progress indicator. The test will automatically close when the maximum time limit is reached.

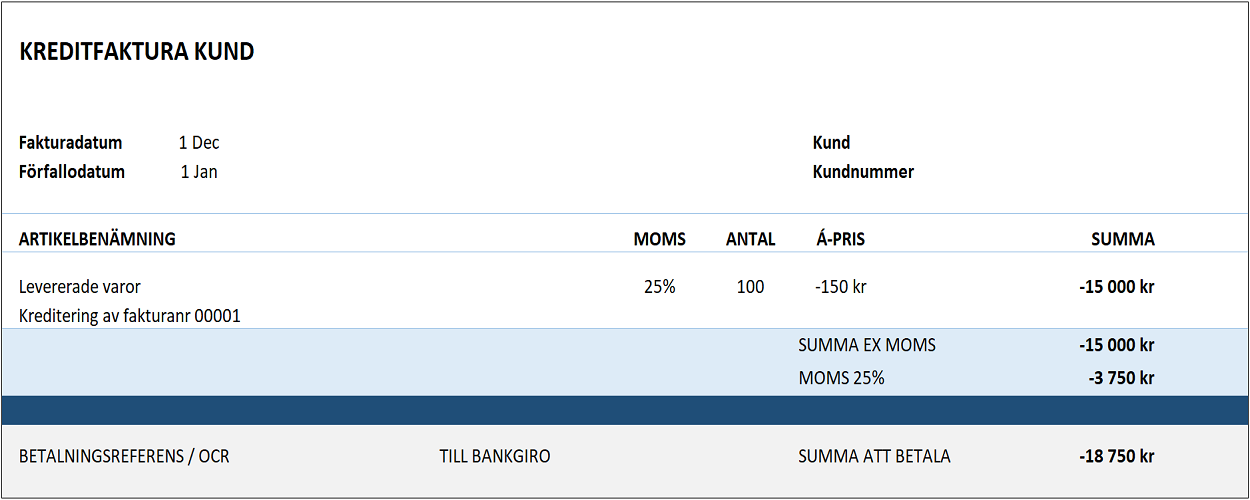

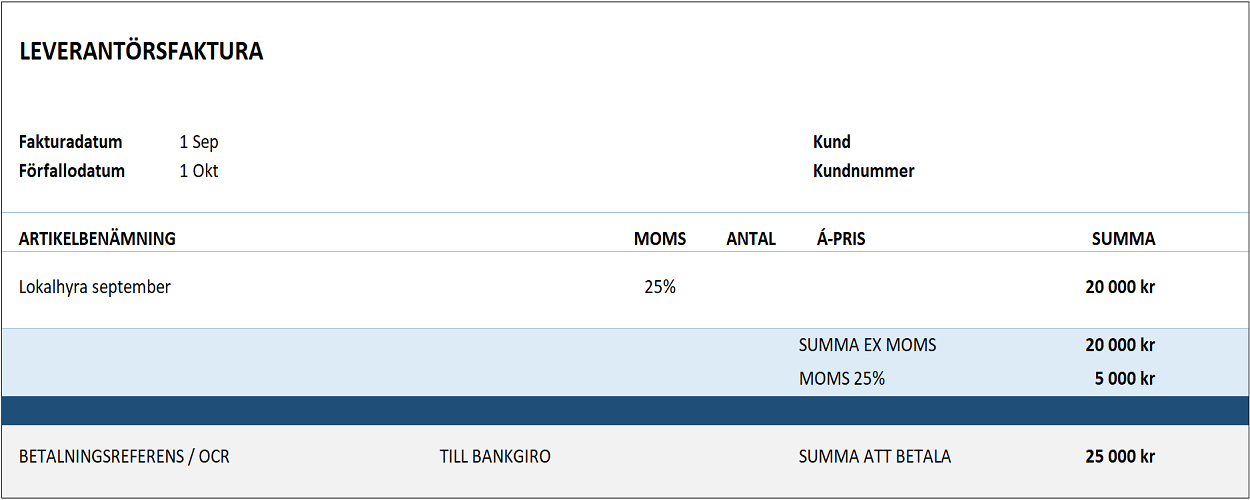

Test questions and answer options can consist of text, images, or a combination of text and images.

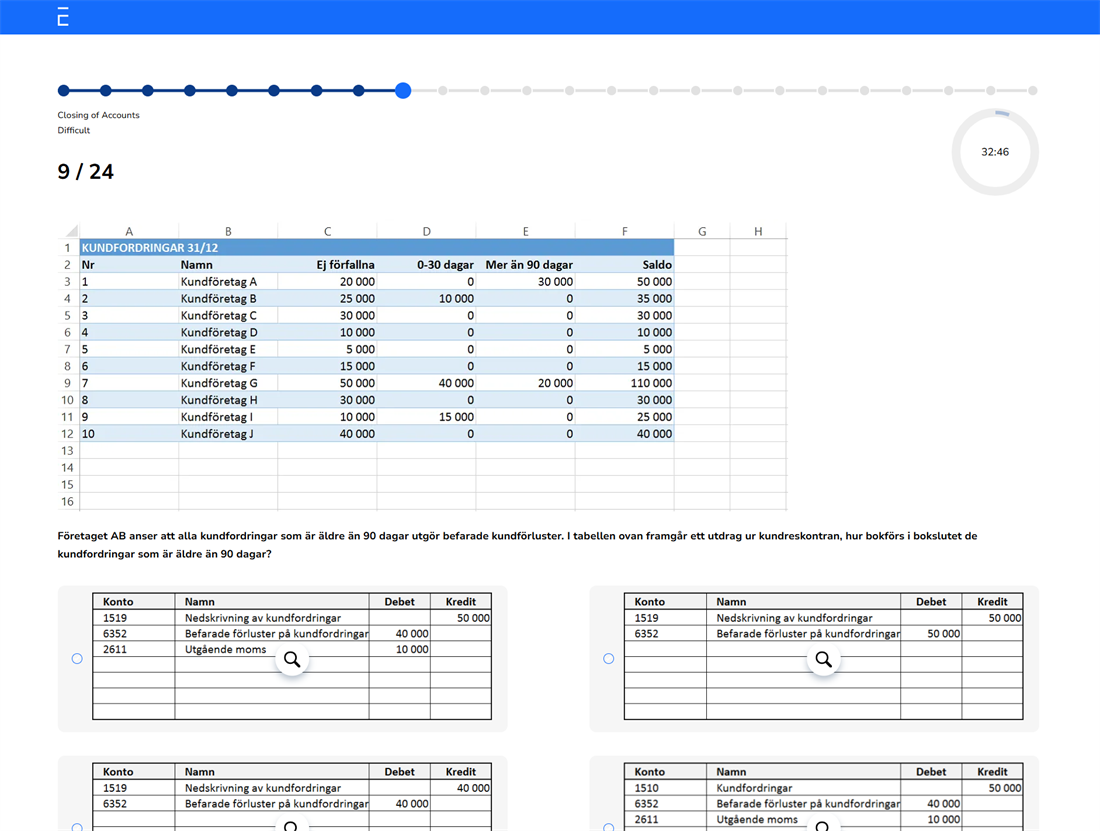

Example Question