TEST AREAS

"ACCOUNTING FROM A TO Z"

Test in English on Swedish GAAP. Differentiates qualified accountants from support profiles handling day-to-day accounting.

Questions and answer choices are in English to facilitate reading comprehension for candidates whose native language is not Swedish. However, images, accounting boxes, etc., remain in Swedish.

Bookkeeping

Testing of both basic bookkeeping, e.g. common customer and supplier invoices, representation and receipts, correction of a recorded transaction, credit invoices etc, to more advanced accounting - e.g. salaries, accrued vacation pay, invoices in foreign currency, tax revenues, etc.

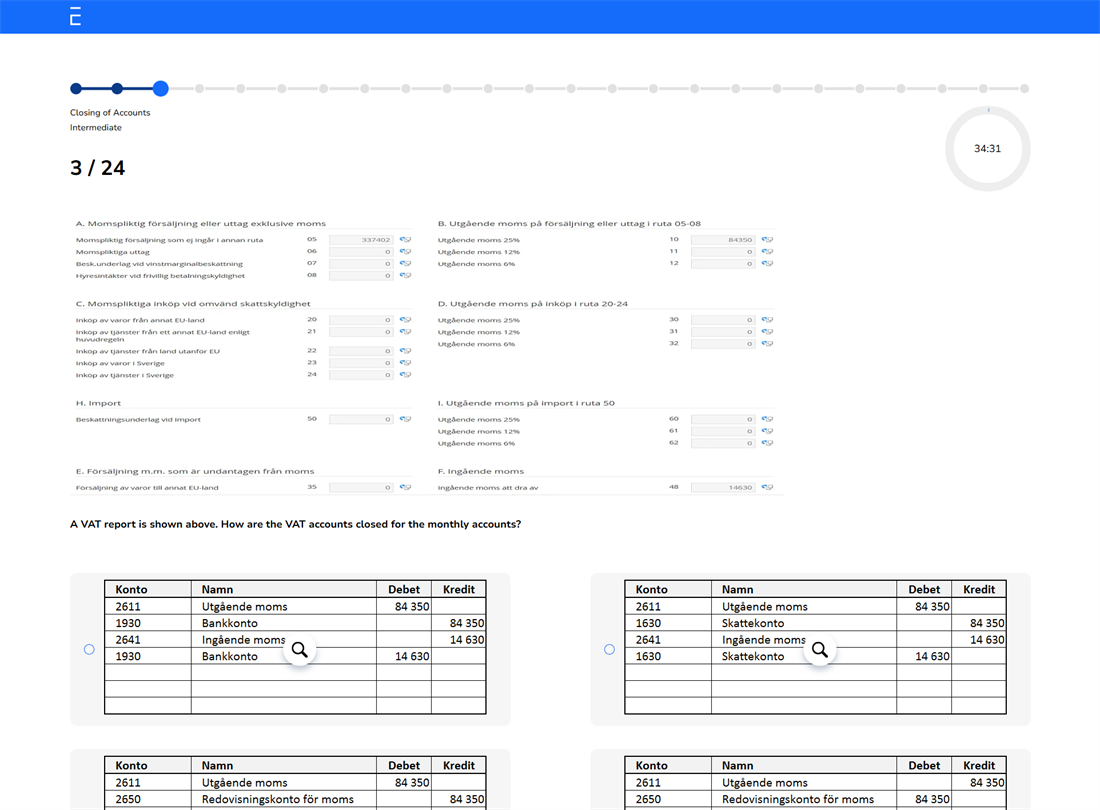

Closing of Accounts

The candidate's knowledge regarding account reconciliations, accruals, various interim accounts and skills in closing VAT accounts, accrual of invoices, recording of taxes and inventory, computation of taxable income, and accounting for anticipated and recognised customer losses, among other things.

Fixed Assets

The candidate's knowledge regarding various types of fixed assets, fixed asset registers, depreciation and write-downs, tax depreciation, main and supplementary rules (SV: Huvud- och Kompletteringsregeln), consumable inventories, goodwill, impairment testing under IFRS, calculation of capital gains, etc.

Accounting Theory

Understanding the meaning and purpose of verifications, monthly reconciliations, accruals, accrued and prepaid items, definitions of revenue and expenses, consolidated financial statements, elimination of internal transactions, percentage of completion, significance of various accounting principles, indirect method regarding cash flow, IFRS vs. K3 regarding financial instruments, and useful life for intangible assets, among others.

TEST QUESTIONS

Multiple Choice and Manual Entry Questions

Our tests are mainly based on multiple-choice questions where the number of correct answer options varies. Each question has four answer options. Some questions require manual recording of a business transaction, and the candidate is provided with a chart of accounts for assistance.

Questions by Area and Difficulty

The tests are divided into four question areas and questions are categorised into three difficulty levels: easy, intermediate and difficult.

Randomised Test Generation

Questions within each area and difficulty level are randomly selected from a question bank, ensuring that each test receives a unique set of questions. Additionally, the order of answer options is randomised so that the correct answer for each question never appears in the same position.

24 Questions and Multimedia Options

A total of 24 questions are generated and must be answered within 35 minutes. During the test, candidates can skip questions and come back to them later. They also have access to a timer and a progress indicator. The test will automatically close when the maximum time limit is reached.

Test questions and answer options can consist of text, images, or a combination of text and images.

Example Question